Homebuyers and homeowners alike are asking: why are mortgage rates going up? This question has become increasingly relevant as interest rates fluctuate in response to economic conditions. Rising mortgage rates can affect affordability, monthly payments, refinancing opportunities, and overall financial planning.

In this comprehensive guide, we’ll explore why are mortgage rates going up, break down the economic and financial factors, examine historical trends, provide examples, and answer frequently asked questions to help you understand the current mortgage market.

Understanding Mortgage Rates

Before diving into why are mortgage rates going up, it’s important to understand what mortgage rates are. A mortgage rate is the interest charged on a home loan. It determines your monthly payment for principal and interest and affects the total cost of the loan over time.

Mortgage rates are influenced by:

- Economic conditions

- Federal Reserve policies

- Inflation

- Housing demand

- Credit risk and borrower profile

Even small rate changes can have a significant impact on affordability.

Current Mortgage Rate Trends in 2026

As of April 2026, average mortgage rates are higher than they were in recent years:

| Loan Type | Average Rate | Term |

|---|---|---|

| 30-Year Fixed | 6.25% | 30 years |

| 15-Year Fixed | 5.75% | 15 years |

| 5/1 ARM | 5.95% | Adjustable after 5 years |

These rising rates have prompted many borrowers to ask: why are mortgage rates going up, and how will it impact their home purchases?

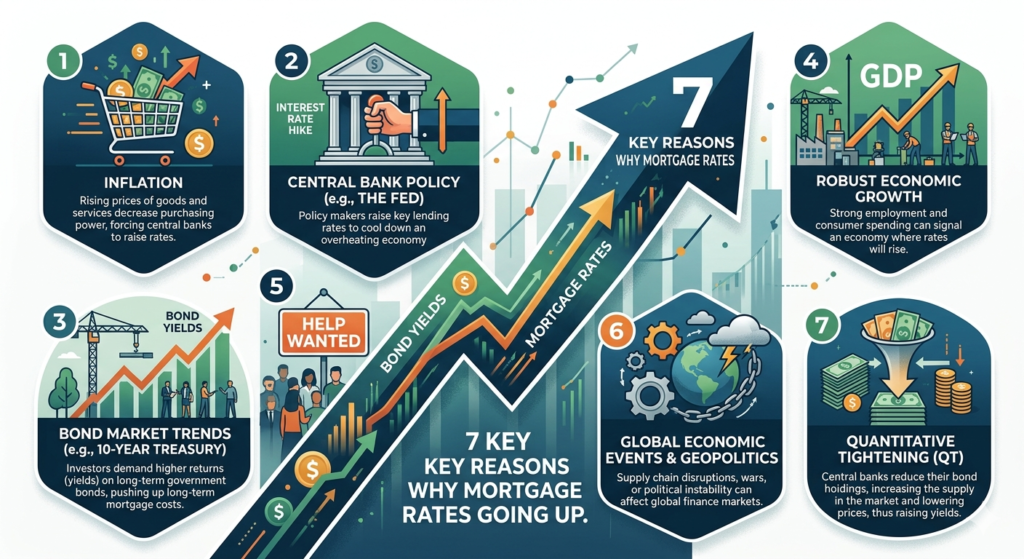

1. Inflation

One of the main reasons why are mortgage rates going up is inflation.

- Inflation reduces the purchasing power of money.

- Lenders raise rates to maintain real returns on loans.

- The Federal Reserve may increase benchmark interest rates to combat high inflation, which indirectly pushes mortgage rates higher.

Example:

| Inflation Rate | Mortgage Rate Impact |

|---|---|

| 2% | Stable rates |

| 4% | Moderate increase |

| 6%+ | Significant rate hike |

2. Federal Reserve Policy

Another key factor in why are mortgage rates going up is the Federal Reserve’s monetary policy:

- Fed sets short-term rates, which influence long-term borrowing costs.

- When the Fed raises rates to control inflation, mortgage rates tend to rise.

- Conversely, rate cuts can reduce mortgage rates, though not immediately.

3. Economic Growth and Demand

Strong economic growth often leads to higher mortgage rates:

- Increased demand for credit drives up rates.

- Higher employment and wages can boost inflation expectations, prompting lenders to increase rates.

- Robust housing market activity often correlates with rising mortgage rates.

4. Global Financial Markets

Global economic events also affect why are mortgage rates going up:

- Investors seek safe assets like U.S. Treasury bonds.

- Rising yields on government bonds increase mortgage rates, since mortgages are often tied to long-term bond yields.

- Geopolitical instability or global inflation can indirectly affect U.S. mortgage rates.

5. Housing Market Conditions

The housing market itself influences why are mortgage rates going up:

- High home prices can lead lenders to raise rates to mitigate risk.

- Low inventory with strong buyer demand can push mortgage rates slightly higher.

- Regional variations in property taxes and insurance costs may influence lender pricing.

6. Credit Risk and Borrower Profiles

Mortgage rates also reflect the perceived risk of borrowers:

| Credit Score | Rate Impact |

|---|---|

| 760+ | Lowest rates |

| 700–759 | Slightly higher |

| 650–699 | Above average |

| Below 650 | Higher rates, more restrictions |

Borrowers with lower credit scores contribute to higher average rates as lenders price in risk.

7. Historical Perspective

Looking at history helps understand why are mortgage rates going up and what drives long-term trends:

| Year | 30-Year Fixed Avg Rate |

|---|---|

| 2000 | 8.05% |

| 2005 | 5.87% |

| 2010 | 4.69% |

| 2015 | 3.85% |

| 2020 | 3.11% |

| 2023 | 6.20% |

| 2026 | 6.25% |

Rates fluctuate with economic cycles, inflation, and monetary policy, explaining the current upward trend.

How Rising Rates Affect Homebuyers

Understanding why are mortgage rates going up is important because higher rates impact affordability:

| Loan Amount | Rate | Monthly Payment | Notes |

|---|---|---|---|

| $300,000 | 5.5% | $1,703 | Lower rate, lower payment |

| $300,000 | 6.25% | $1,845 | Current rate, higher payment |

| $300,000 | 7% | $1,996 | Hypothetical further increase |

Even a 0.5% increase can add hundreds of dollars to monthly payments.

Strategies for Homebuyers

To mitigate the impact of rising rates:

- Lock in Rates Early: Pre-approval with a rate lock protects against further increases.

- Consider Adjustable-Rate Mortgages: ARMs can offer lower initial rates.

- Improve Credit Score: Better scores may qualify for lower-than-average rates.

- Increase Down Payment: Reduces loan principal and monthly payments.

- Shop Lenders: Compare rates and fees from multiple sources.

FAQs on Why Are Mortgage Rates Going Up

Q1: Why are mortgage rates going up so fast?

A1: Rapid rate increases are often due to rising inflation, Federal Reserve hikes, and strong economic growth.

Q2: Will mortgage rates continue to rise?

A2: Future rates depend on inflation trends, Fed policies, and global economic conditions.

Q3: How do rising rates affect home affordability?

A3: Higher rates increase monthly payments and reduce the amount of home you can afford.

Q4: Can I refinance if rates are rising?

A4: Refinancing may be less beneficial during rising rates; locking in lower rates early is ideal.

Q5: Are adjustable-rate mortgages better in this environment?

A5: ARMs can offer lower initial payments, but may rise if market rates continue to increase.

Q6: How do global events influence U.S. mortgage rates?

A6: Investors adjust their bond holdings, which affects U.S. Treasury yields, indirectly influencing mortgage rates.

Conclusion

Understanding why are mortgage rates going up is essential for both prospective homebuyers and current homeowners. Inflation, Federal Reserve policies, economic growth, global markets, housing conditions, and borrower credit all contribute to rising rates.

By staying informed, improving credit, comparing lenders, and planning strategically, you can mitigate the effects of higher mortgage rates and make confident financial decisions. Monitoring these factors ensures you are prepared to navigate the housing market despite rate fluctuations.